[ad_1]

Global investment banking firm Jefferies sheds light on the remarkable turnaround of India’s public sector undertakings (PSUs) in the past 12 months, marking a significant departure from a decade of underperformance before 2020.

PSU index has risen, outperforming Nifty

Jefferies emphasizes that despite this recent rise, the PSU index is still trading at a substantial 40% discount to the Nifty, presenting a compelling 15% upside potential to reach the average level. A key factor contributing to this resurgence is the government’s modified stance towards “value maximization” for state-owned enterprises (SOEs).

The report highlights three of the top PSU options identified by Jefferies: State Bank of India

In calendar year 2023, the PSU index outperformed the Nifty by 40%, with a further 15% outperformance recorded so far this year. The rally across the PSU spectrum is attributed to both accelerated capital spending by the government and sector-specific factors.

Despite the strong performance, the price-earnings (PE) ratio of the PSU index stands at 12.1 times, which is a 40% discount to the Nifty. This compares with an average discount of 31% before FY18 in Nifty PE, indicating potential scope for further revaluation.

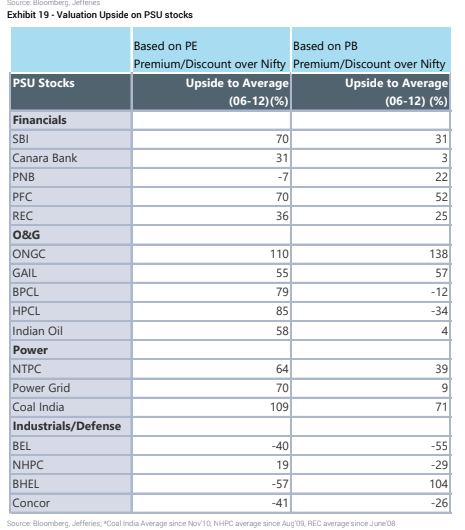

Jefferies draws attention to historical valuations, suggesting that PSU banks, power/coal companies and certain oil and infrastructure companies had significantly higher multiples during the 2006-2012 period.

The RoE of PSUs had earlier fallen to 4-6% from the range of 14-15%, mainly due to challenges faced by PSU banks. However, with the recovery of profitability, the RoE has improved again to 12-13%, with expectations of further improvement.

Most PSUs have seen substantial improvements in EPS, although exceptions include ONGC, Concor and BHEL.

The PSU banks index has risen 78% year-on-year, outperforming private banks by 70%. This impressive performance is attributed to a strong earnings recovery, driven by improvements in asset quality and attractive valuations.

PSU banks have also enjoyed lower loan-to-deposit ratios, which has facilitated competitive loan growth. In FY24, PSU bank credit growth is only 2-3 percentage points behind private banks, a significant improvement from the pre-COVID gap of 8-10 percentage points.

Comparing PSU Bank’s valuations to the 2006-2012 period, marked by strong fundamentals and a rising capex cycle, Jefferies suggests 25-30% upside potential on PE/PB valuations, in addition to returns expected normals based on 15% RoE capitalization. % or more.